How Paytm Money accelerates wealth creation with its Direct Mutual Funds offering?

India's homegrown digital financial services platform Paytm's wholly-owned subsidiary Paytm Money is empowering its users with Direct Mutual Funds offerings to accelerate wealth creation. There are two options available through which one can invest in Direct & Regular. When one goes through a distributor, broker, or bank, it is usually a regular mutual fund. As one might not be aware, mutual fund distributors get paid commissions thus returns can be lesser if one opts for the Regular option. Investors can earn around 1% higher return on investment by opting for Direct Funds. Paytm Money offers easy onboarding, a seamless investing experience, and the widest range of choices to its users.

For instance, if you invest Rs. 1 lakh in Aditya Birla Sun Life Mid Cap Fund through Regular route the expense ratio is 2.15%, whereas if you invest through the Paytm Money app the expense ratio is 1.21%. An investor would yield the returns of 10.9%if you invest through direct & 9.9% if you invest through regular.

Varun Sridhar, CEO, Paytm Money said, “Our intention to offer direct mutual funds for free i.e without incurring any commissions and with a fully transparent approach is to gain investor trust. Investing in direct mutual funds through Paytm Money will increase your returns by around 1% as opposed to regular schemes.”

Here is why investing in Direct Mutual Funds makes sense.

For the uninitiated, the Mutual Fund Industry in India has grown rapidly over time, with the Asset under Management (AUM) growing from INR 90,587 crore in March 31, 2001 to Rs 29.83 lakh crore as of November 2020. But even as the AUM burgeoned to massive proportions, it was observed that the retail investors were not receiving the benefits of scale. So, in order to protect the interest of retail investors, SEBI came forth in October 2018 and rationalized the Total Expense Ratio (TER) of mutual funds.

SEBI witnessed that even though there were substantial TER cuts with fund size expansion in the non-equity segment, which was populated by the institutional investors. However, a similar kind of transfer of the benefit of lower TER wasn’t conspicuous in equity-oriented mutual funds that were the main resort of retail investors.

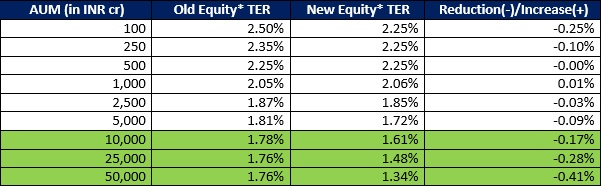

How is New TER structure different from the Old one?

You would probably be aware of how investing in direct mutual funds can result in higher returns owing to lower TER as compared to regular mutual funds. Here, we shall take a deeper dive into how the recent cuts in the TER in direct funds itself by SEBI would enable you to accumulate higher wealth in the long run.

Given below is a table showing the effective TERs of equity-oriented schemes according to the old structure and the new structure that became effective from April 1, 2019, and highlighting the variation in the overall expenses.

Note: * denotes all equity-oriented mutual funds i.e. schemes that have more than 65% exposure to equities.

How would you be benefitted from this?

The overall NAV of the fund is reflected after taking into account the expenses. So, a lower TER would mean a lesser burden on the fund NAV & higher returns for you that when reinvested would bulk up into a bigger corpus in the future.

Even though the reduction in the TERs by few basis points might seem insignificant at the first instance, but over time with the benefit of compounding, it will make a huge difference to your portfolio.

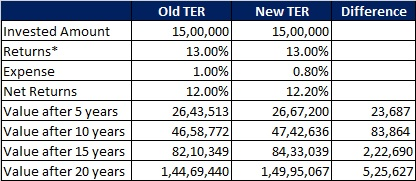

Let’s take an illustration to understand this better.

Note: Amounts are in INR. * denotes 20 year average annualized returns for Large cap funds

A mere 20 basis point change in TER can earn you over Rs 5 lakh more over a period of 20 years.

The expense ratio of the Direct Plan is always lesser than the Regular Plan for the same mutual fund scheme. By switching from Regular Plans to Direct Plan of mutual fund schemes you can make sure that you keep earning more on your investment!

As switch transaction involves redeeming units from the regular plan and making a fresh investment in a direct plan, exit load (if any) and capital gains tax would apply.

In the case of equity funds, if you switch within 1 year from the date of investment, the Short Term Capital Gains (STCG) will be taxed at 15% plus an applicable surcharge. However, if you switch after 1 year from the date of investment, then the Long Term Capital Gains (LTCG), exceeding the threshold of Rs 1lakh, will be taxed at 10% plus an applicable surcharge.

In the case of debt funds, if you switch within 3 years from the date of investment, then the STCG will be taxed as per your applicable slab rates. However, if you switch after 3 years from the date of investment, then the LTCG will be taxed at 20% after indexation benefit.

At Paytm Money, you can switch from regular to direct plan in a few easy steps & with a fully digital KYC.